Tata Steel, the flagship steelmaker in Tata Steel, the flagship steelmaker of Tata Group, continues to establish itself as a leader in the steel industry worldwide. In the first quarter of FY26 (ending June 30th 2025) it’s Indian production facilities generated 5.26 million tons of steel in crude form, a flat year-on-year growth. Meanwhile, European production increased only slightly (~+2 percent YoY) even with maintenance shut-downs. Revenues from India operations grew by 3 percent YoY to reach Rs34,901 crore, even though EBITDA fell by Rs15,651/tonne) because of high input costs. Globally, however overall revenue surged ~18.6 percent YoY to reach Rs63,430 crore and EBITDA margin rising to 22,717/tonne). However the the consolidated PAT fell by 65-92 percent YoY to the sum of Rs634 crore. This was a result of the deferred tax and pension cost. Tata Steel also approved a capex budget of Rs15,000 crore for FY26 and 80% of it is earmarked to fund India capacities expansion. These diverse themes — production stability margin pressure, concerns about profitability and investment drives–define the steel giant’s strategic crossroads.

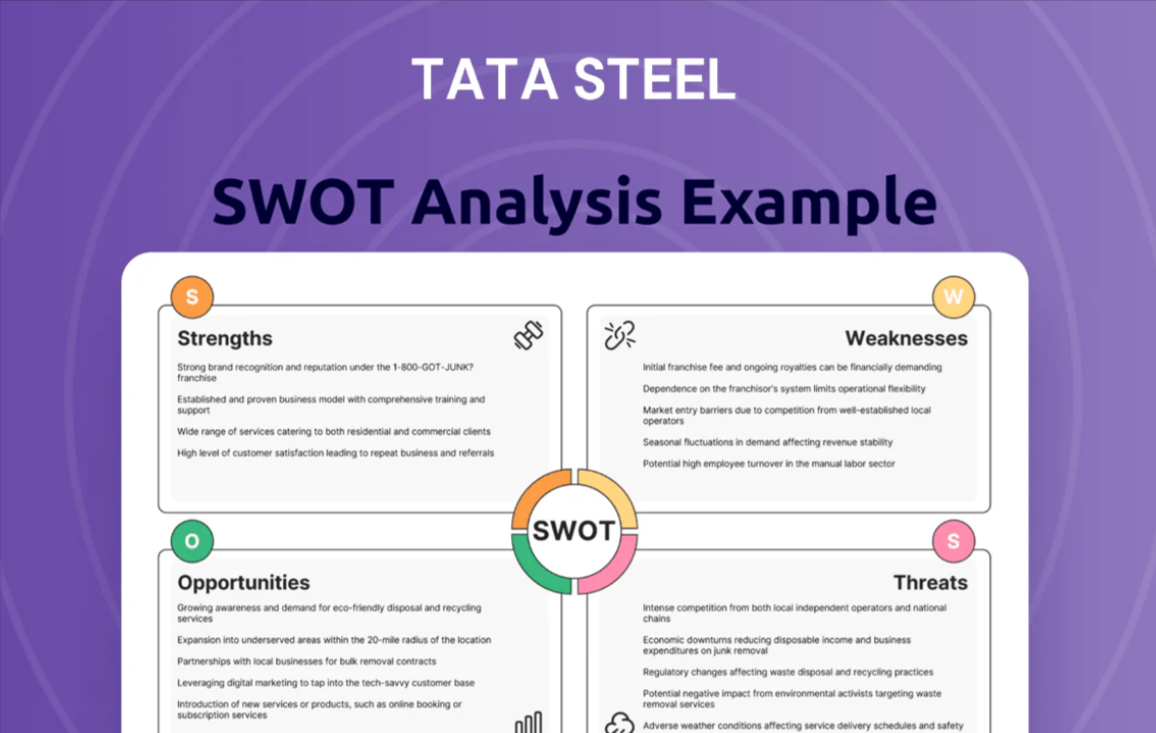

Strengths

1. Global Scale and Global Footprint: With a total annual capacity of 35 million tonnes operating are carried out in India, UK, Netherlands, Thailand, and more, Tata Steel is the second largest and most geographically diverse major steel producer.

2. Captive Supply of Raw Materials India’s first steel plant integrated situated in Jamshedpur and captive mines for ore guarantee price control and stability of supply.

3. Strong Brand & Legacy More than a century of operations and a connection with sustainable development and Indian industrial advancements have built an immense amount of trust to corporates.

4. Cost Efficiency & Vertical Integration Operation supported by steelmaking, mining, downstream processing and R&D–including high-carbon technologies such as HIsarna, which boost margins and strategically placed.

5. A robust Capex Plan: With Rs15,000 cr earmarked for capacity and efficiency-related projects in FY26 Tata Steel is strengthening its long-term competitive structure.

Insufficiencies

1. Profit Volatility: Despite strong operations, the consolidated PAT fell by 65-92% in Q1 FY26 due primarily to tax-related charges in addition to pension obligations.

2. High Input Cost Sensitivity: Margin decline–EBITDA/tonne fell to Rs15,651–signals vulnerability to price swings in coal, iron ore, and energy.

3. European Unit Complexity European Facilities operate on separated value chains and have to pay significant overheads and compliance costs.

4. Technology Adoption Gaps: A few production facilities lack the latest automation technology, however initiatives such as HIsarna indicate a positive direction.

5. Capital Intensity and Leverage Capex that is heavy (~Rs15,000 million) and modernization debt can increase risk if returns are not as high as.

Opportunities

1. The growing demand for domestic steel: infrastructure construction, housing in rural areas as well as auto production in India create a steady steel demand expansion.

2. Advanced Steel & Value-Added Solutions Opportunities are in the premium flat and special steels for automotive, and specialized downstream products.

3. Low-Carbon Technology Advantage: Growing HIsarna and other green technology adoption can help reduce costs along with ESG differentiation.

4. Export and International Market Expanding: Capacity Boost could feed the export markets of Southeast Asia, Middle East and Africa particularly under secure trade conditions.

5. Industries Consolidation M&A both in India and elsewhere (e.g. coal blockages) can provide strategic assets as well as scale gains.

Threats

1. Global Oversupply and Imports: Cheap Chinese imports as well as aggressive policies in foreign markets affect margins and prices at home .

2. Environmental and Regulatory Pressure: Carbon taxes, emission limits and EU regulations increase requirements for compliance.

3. Commodity Price Volatility Sharp swings in Coking coal, iron ore could pose risks to the margins of cyclical commodities .

4. Economic Slowdowns: A slowdown in infrastructure, manufacturing, or auto demand – similar to Europe – could decrease the load and boost the absorption of fixed costs.

5. Trade Barriers and Tariffs Trade actions that are retaliatory such as certifications, zoning, or rules for export markets can restrict growth.

Future Outlook

Margin Rebound and Profit Recovery: With the normalization of input prices and expansion of capacity occurring across India and Europe EBITDA/tonne is anticipated to rise by the end of H2 FY26.

Green Steel as Edge: Scaling HIsarna and low-carbon processes can help position Tata Steel as a premium producer during the global ESG shift.

Domestic Leadership and the growth of exports: Investments in Kalinganagar and other facilities support the growth of local demand as well as export plans.

Diversification of Steel Products: Expansion into automotive-grade steel TMT, coated products and NSPs to support rural infrastructure increases the quality of income.

international asset optimization: Streamlining the high cost European operations and boosting global competitiveness via synergies, cost control along with strategic alliances.

Technological Upgrade: Accelerating automation, digital twin implementation, as well as AI-powered predictive maintenance can boost efficiency and security.

Tata Steel remains a global steel giant, but it faces an immediate assessment of the stability of its margins due to macro-cost pressures. Implementation of its green-tech strategy as well as expansion in the domestic market along with export optimization and operational re-alignment will determine if it transforms its capacity into sustainable, profitable growth. This keeps its place as a leading company in the new decarbonized steel age.